At the end of the second quarter of 2024, the MINING.COM TOP 50* ranking of the world’s most valuable miners had a combined market capitalization of $1.43 trillion, up $42 billion from end-March, as rising copper and gold prices make up for losses among lithium and iron ore counters.

Gold and copper’s historic runs to new all-time highs in May arguably should have sparked a bigger rally during the quarter and year-to-date but mining’s top tier is only worth little over 2% more than at the end of last year and an equally uninspiring 6% gain from this time last year.

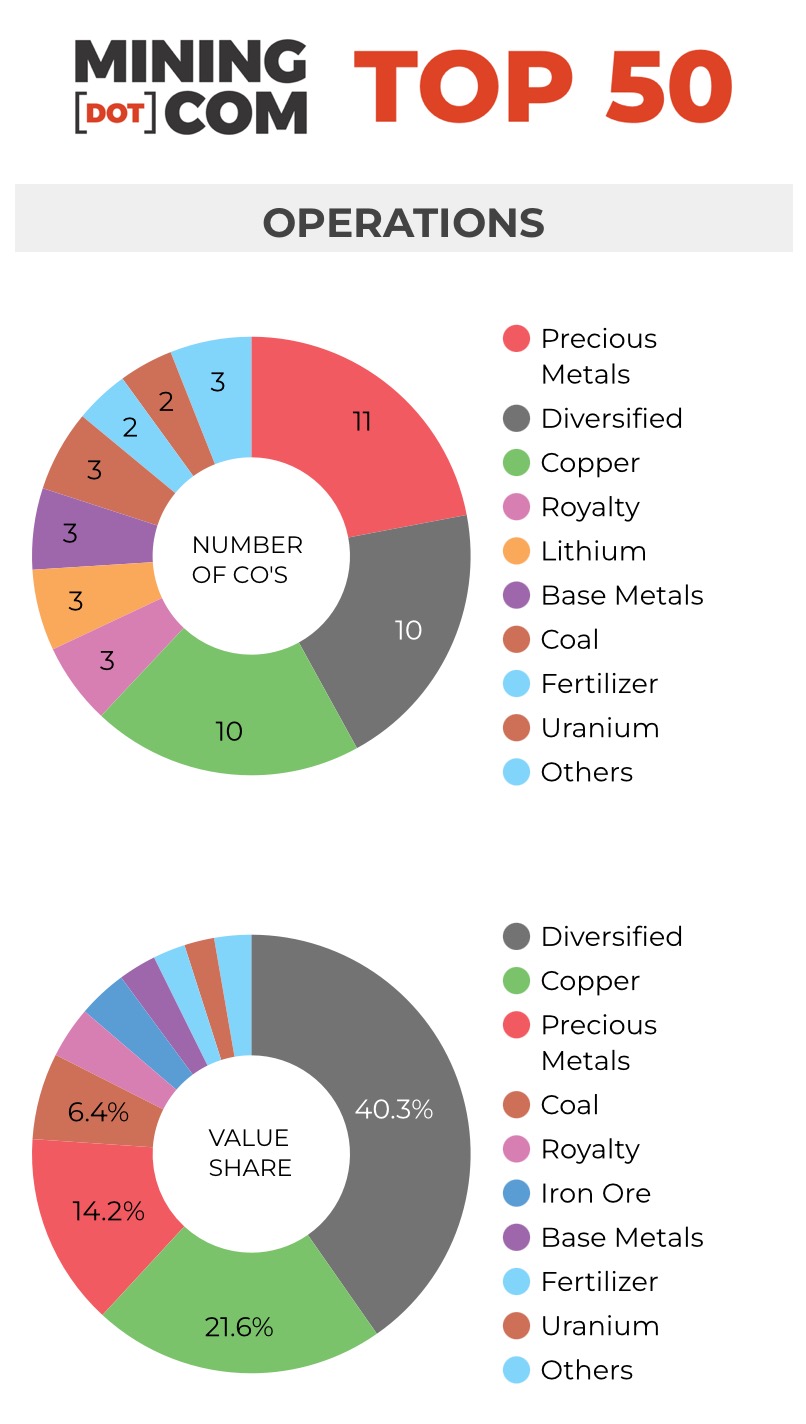

Diversified drubbing

Copper specialists have gained a combined 33% year to date but the industry’s traditional big 5 – BHP, Rio Tinto, Glencore, Vale and Anglo American – have lost a collective $59 billion since the start of the year.

The boost from copper was also not enough to counter iron ore’s descent into bear territory from dragging down the group, which now make up 29% of the total index, down from a height of 38% at the end of 2022. The steelmaking ingredient’s less than rosy outlook also sees two specialists – Cleveland Cliffs and Fortescue – appear in the worst performer list.

Were it not for Glencore’s lack of exposure to iron ore other than through trading, steadying the Swiss giant’s share price, and Anglo American’s 25% jump during the quarter on the back of BHP’s unsuccessful takeover bid, mining’s traditional heavyweights would be an even more diminished grouping.

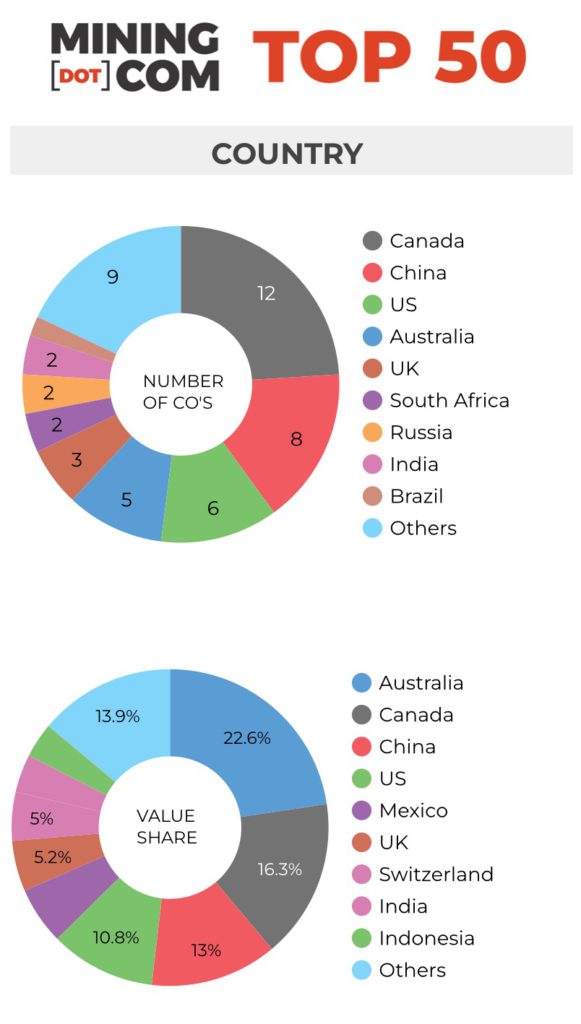

Investors in Anglo, with a history going back more than a hundred years on the South African gold and diamond fields, have had a particularly wild ride over the last few years. In January 2016, Anglo’s market cap fell below $5 billion and even after the stock’s Q2 bump, is still only worth half its peak valuation hit in 2022.

While the BHP takeover is unlikely to be revived, M&A among the top of the mining industry seems inevitable, particularly when copper is involved, given the billions of dollars of capital expenditure needed for expansion and just to keep operating mines ticking over, to meet demand for the metal through the next decade.

Light on lithium

Three counters dropped out of the top 50 during the first quarter – Brazil’s CSN Mineração, an iron ore miner, China’s Huayou Cobalt and Australian lithium producer Pilbara Minerals.

At the end of Q2, two more lithium stocks – Perth-based Mineral Resources and China’s Tianqi Lithium – exited the top 50 as the deep slump in prices for the battery metal continues to take its toll.

Mineral Resources was only just pipped by Ganfeng Lithium and based on its performance so far in July, the Australian hard rock lithium miner may well return to the fold.

Ganfeng was barely holding on at position 50 at end-June and with gold price momentum continuing and two gold mining companies waiting in the winds – Yintai and Alamos – only three lithium counters in the top 50 may be a reality for some time to come.

After peaking in the second quarter of 2022 with a combined value of nearly $120 billion, the remaining lithium stocks’ market value now barely exceeds $30 billion.

Can’t top copper

Copper, gold producers and royalty companies made up 40% of the index at the end of Q2 on par with diversified miners as Pan American Silver, following its absorption of Yamana Gold enters the ranking for the first time and Polish copper giant KGM returns after adding 17% to its market cap during the quarter.

Talks of a possible reopening of its Panama mine saw First Quantum Minerals’ market valuation nearly doubling in US dollar terms from its low at the end of last year, and the Vancouver-based company is now firmly back in the ranking at #34 after dropping out at the end of last year.

Amman Mineral continues its run up, piercing the top 10 for the first time after gaining 67% year to date, and 580% since its debut in Jakarta a year ago, lifting the copper-gold company’s market cap to over $50 billion.

Amman’s Batu Hijau is the third largest mine worldwide in terms of copper equivalent output and has been in production since the turn of the millennium. Amman is also developing the adjacent Elang project on the island of Sumbawa.

Radiant uranium

While spot uranium prices have retreated back below the triple digit prices hit in January, the combined market cap of the sector is still up 42% from last year this time and together now surpasses that of the lithium counters in the ranking.

The world’s largest uranium producers – Cameco and Kazatomprom – only made the top 50 in 2021 with the Saskatoon-based company and state-owned Kazakh producer spending years in the wilderness post the Fukushima disaster in Japan.

None of the smaller uranium companies led by Canada’s Nexgen Energy, valued at a shade over $4 billion, is likely to make it into the top 50 by themselves, but combinations among the rank and file may well be in the offing as interest in the sector and mining M&A in general grows.

Kazatomprom dual-listed in London and Astana in 2018 and Uzbekistan is readying an IPO for Navoi Mining and Metallurgy Combinat – the world’s fourth largest gold mining company and significant uranium producer later this year.

Navoi would join the ranks of gold producers in the top 50 thanks to ownership of the world’s largest gold mine, Muruntau, and annual production of 2.9 million ounces at grades the envy of the sector. Navoi will also bring to five the number of companies with exposure to the nuclear fuel in the ranking.

Notes:

Source: MINING.COM, stock exchange data, company reports. Share data from primary-listed exchange at close July 1, 2024 close of trading converted to US$ where applicable. Percentage change based on US$ market cap difference, not share price change in local currency.

As with any ranking, criteria for inclusion are contentious. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information. That, of course, excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining (the gold and uranium giant may list later this year), Eurochem, a major potash firm, and a number of entities in China and developing countries around the world.

Another central criterion was the depth of involvement in the industry before an enterprise can rightfully be called a mining company.

For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or warrant a seat on the board?

This is a common structure in Asia and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec.

Levels of operational or strategic involvement and size of shareholding were other central considerations. Do streaming and royalty companies that receive metals from mining operations without shareholding qualify or are they just specialised financing vehicles? We included Franco Nevada, Royal Gold and Wheaton Precious Metals on the basis of their deep involvement in the industry.

Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy or Bayan Resources where power, ports and railways make up a large portion of revenues pose a problem. The revenue mix also tends to change alongside volatile coal prices. Same goes for battery makers like China’s CATL which is increasingly moving upstream, but where mining will continue to represent a small portion of its valuation.

Another consideration is diversified companies such as Anglo American with separately listed majority-owned subsidiaries. We’ve included Angloplat in the ranking but excluded Kumba Iron Ore in which Anglo has a 70% stake to avoid double counting. Similarly we excluded Hindustan Zinc which is listed separately but majority owned by Vedanta.

Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and many others.

Head office refers to operational headquarters wherever applicable, for example BHP and Rio Tinto are shown as Melbourne, Australia, but Antofagasta is the exception that proves the rule. We consider the company’s HQ to be in London, where it has been listed since the late 1800s.

Please let us know of any errors, omissions, deletions or additions to the ranking or suggest a different methodology.