- Despite a sharp decline in Saudi GDP in FY23, FY24 is expected to see a return to >4% growth.

- The Kingdom is expected to continue its diversification away from hydrocarbons with investment in key sectors from both the PIF and NIS.

- Despite a fall in M&A activity in the Kingdom in 2023, a positive economic outlook and a myriad of investment opportunities suggests a rebound in deal activity and an increase in deal value in 2024.

- Five key sectors are expected to offer the most exciting M&A opportunities in the Kingdom this year: mining, energy, technology, gaming and esports, and infrastructure.

2023 in Review

2023 was characterised by a shift in the global macroeconomic regime, with inflation rising across developed economies and central banks responding with several rounds of monetary tightening.

These unsettling effects were exacerbated by unfolding geopolitical schisms in Ukraine and the Middle East, with the former disrupting global supplies of essential agricultural commodities and the latter leading to a shipping crisis in the Red Sea.

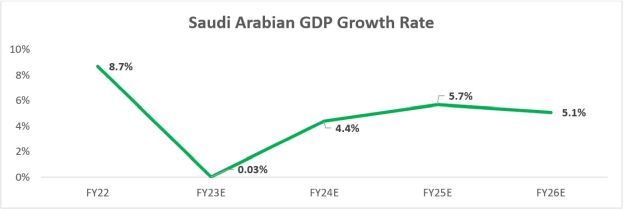

The Kingdom of Saudi Arabia was not immune from these economic headwinds. According to current GDP projections from the International Monetary Fund (IMF), FY23 is expected to see growth of only 0.8% in the Kingdom’s output. The Saudi Ministry of Finance (MoF) is less optimistic, forecasting a meagre 0.03%, down from 8.7% growth in FY22 (see figure 1). This contraction can be attributed to a decline in oil production, offsetting gains from non-oil economic activity.

Figure 1: Data taken from the MoF, December 2023.

Despite the sharp fall in output, not all economic news for the Kingdom was negative. Both inflation and unemployment remained low, consumer spending rose steadily throughout the first three quarters of the year (data for Q4 currently unavailable), and activity in the non-oil private sector continued to expand.

The Kingdom has also continued pursuing its Vision 2030 objectives, with the aim of diversifying the economy away from its reliance on international oil sales. Between 2012 and 2022 the contribution of hydrocarbons to the economy fell from 45% to 40%. Growth in the manufacturing, tourism and hospitality sectors has driven this decline.

Central to the Kingdom’s continued diversification efforts are the National Investment Strategy (NIS) and the Public Investment Fund (PIF) which have continued to invest heavily in a range of industries, including logistics, transport, mining, and clean technology.

Notable legislative reform also took place in 2023. In June 2023, Saudi Arabia introduced the Civil Transactions Law, which represents a significant milestone in the codification of Saudi law. The new legislation, inter alia, plugs the legislative gap that had previously existed in relation to the regulation of legal contracts, and aims to provide greater certainty to individuals and companies doing business in the Kingdom.

This followed the introduction of the new Companies Law in January 2023, which regulates all forms of entities in the Kingdom and seeks to align corporate law with Vision 2030 objectives. Like the Civil Transaction Law, the new Companies Law demonstrates a willingness to pursue reforms necessary to enhance the attractiveness of the Kingdom to foreign investors.

2024 Economic Outlook

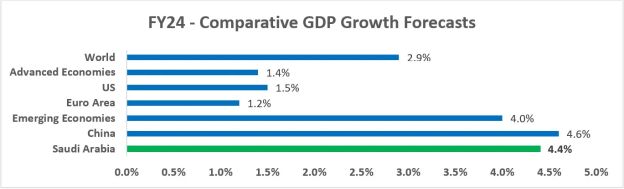

Expectations for FY24 are more buoyant, with forecasts of 4% (IMF), 4.4% (MoF), and 4.6% (Moody’s). These figures are largely consistent with expectations for emerging economies, with the MoF predicting 4% growth across this cohort (see figure 2).

Figure 2: Data taken from the MoF and Aljazira Capital, December 2023.

Several factors are propelling this growth. The first is a return to a more hospitable monetary regime, with the Saudi Arabian Monetary Authority (SAMA) expected to cut the repo (repurchase) rate by 100 basis points. This fall in rates – combined with similar falls in the United States, United Kingdom, and European Union – could increase liquidity and attract further foreign investment into some of the Kingdom’s megaprojects (e.g. NEOM, Red Sea Project). The reduction in interest rates suggests that inflation will also decline. This monetary shift, in concert with corporate profit growth, also creates a positive outlook for the Tadāwul (stock exchange), with Aljazira Capital forecasting a ~10% rise in the stock market.

Throughout FY24, consumer spending is expected to increase. Indeed, the banking, retail, technology, tourism, and consumer services sectors all have positive outlooks. Unemployment is forecast to fall at the same time as non-oil private sector activity expands.

Combined with the legislative reforms discussed above (with further reforms expected), the Kingdom also continues to foster a more favourable environment for foreign direct investment.

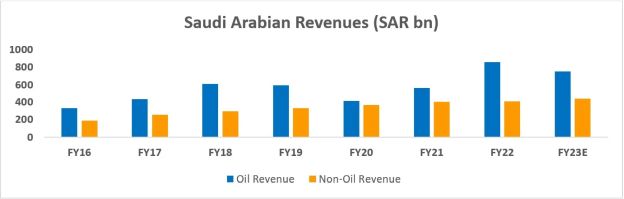

Central to understanding the trajectory of the Saudi economy is the international oil market and its supply and demand dynamics. Non-OPEC members – namely the United States – increased global supply by 1.6 million barrels per day (mbpd) in FY23. This trend is expected to continue, with an extra 1.4 mbpd forecast for FY24. This increase in supply is a response to growing demand from a recovering China, and expectations of a weaker U.S. dollar buoying emerging market economic activity. There are also inflationary risks associated with ongoing turbulence in the Middle East and the current shipping crisis playing out in the Red Sea. However, despite rising supply from non-OPEC states, recent forecasts suggest that demand will comfortably exceed supply. OPEC’s expected supply reduction may exacerbate this shortfall. Whilst analysts have predicted oil prices to remain between US$80 and US$85 a barrel, OPEC is well placed to exert inflationary pressure if needed. This could reverse the fall in oil revenues seen in FY23 (see figure 3).

Figure 3: Data taken from Aljazira Capital Research, December 2023.

Focus Sectors in 2024

Across a range of industries and sectors within Saudi Arabia one can find reasons to be optimistic about the 2024 M&A market. There is significant liquidity within the Kingdom and a resource pool deep enough to support M&A activity. However, the following five key sectors are expected to offer the most exciting opportunities in 2024. As can be seen, each of these sectors is central to Vision 2030.

- Mining: With estimated unexplored mineral wealth of US$2.5 trillion, the Saudi government wants to attract US$200 billion of investment by the end of the decade to develop its nascent mining sector into a key pillar of the Saudi economy. The Mining Investment Law, introduced in 2021, is intended to make it easier to obtain exploration licenses in the Kingdom, helping to create a favourable M&A environment. A US$182 million mineral exploration incentive program was recently announced at the Future Minerals Forum, with up to 30 large mining exploration licenses on offer to international investors in 2024. We expect this to act as a catalyst for further M&A activity in this sector in 2024. Indeed, we are already witnessing extensive mining operations emerge in the Kingdom. For instance, the phosphate mine in Wa’ad Al-Shamal accounts for 2% of Saudi non-oil GDP.

- Energy: Renewable energy is central to the Kingdom’s 2030 Vision ambitions. Crown Prince Mohammed bin Salman has expressed his desire for half of the Kingdom’s electricity to come from wind and solar generation by 2030. The PIF has invested US$50 billion in ACWA Power to support this ambition. ACWA too is pursuing considerable investments both at home and abroad; they expect to triple their level of current investments in green energy assets over the next six years to US$250 billion.

- Technology: The Kingdom is emerging as an exciting place for advanced technology and digital innovation, with billions of dollars of investment planned over the next few years. This includes significant contributions from Oracle (US$1.5 billion), Microsoft (US$2.1 billion), and Huawei (US$400 million) to develop new cloud infrastructure. Domestic support for the sector is already apparent with “Tonomus” – a subsidiary of NEOM – investing US$1 billion in 2022 and Crown Prince Mohammed bin Salman recently launching “Alat”, a new PIF subsidiary, tasked with making Saudi Arabia a global hub for advanced technology manufacturing. Indeed, the Kingdom aims to create 39,000 direct jobs and generate a direct non-oil GDP contribution of US$9.3 billion from this sector by 2030.

- Gaming and eSports: The Kingdom also promises to be an exciting space for gaming and esports, positioning itself as a global hub within one of the fastest growing global industries. Savvy Games Group, a subsidiary of PIF, is charged with delivering this ambitious mandate, with approximately US$40 billion to invest.

- Infrastructure: Perhaps the most active sector in the Kingdom at present is infrastructure. A myriad of giga projects are under development as part of a modernisation effort. The most well-known of these initiatives is NEOM; a new region in the North-West of the Kingdom with an estimated cost of over US$500 billion. Separate from NEOM are additional infrastructure initiatives, including the Red Sea Project – a tourism hub – and Qiddiya – a gaming and esports district.

The scale and speed of the planned expansions across these five sectors offer exciting opportunities for investors both inside and outside the Kingdom in the short-to-medium term and can be expected to generate significant M&A activity in 2024 and beyond.

Combined with an ambitious legislative reform agenda and a palpable optimism in the Kingdom, one feels that, whilst not immune from global economic headwinds, the KSA offers a promising investment outlook in 2024.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.